Optimizing Tender Offers at Stripe

Tender offers at Stripe have become a regular occurrence over the last few years. While there was some temporary craziness in its equity plan, Stripe has emerged as one of the best examples of how to successfully manage equity as a private company and how to carry out tender offers with regularity.

Stripe employees are fortunate. Not every private company gives its employees a chance to sell equity before an IPO. The tricky part is that tender offers typically come with a short window to make decisions, lots of tax complexity, and numerous personal financial decisions that need to be made.

This article will walk you through the process of how to optimize your participation in a Stripe tender offer.

We'll show you how to get organized beforehand, address important tax implications, provide example spreadsheets, offer tips for making smart selections, and give guidance on how to handle the tax aftermath of whatever decisions you make.

If you do the work we outline below, you'll be better prepared for the next inevitable Stripe tender offer.

Table of Contents ▼

Get Organized Before The Stripe Tender Offer

The first thing you’ll want to do is organize the Stripe equity you have. The biggest mistake Stripe employees make is waiting until the last minute. Getting organized ahead of time makes the pressure associated with a tender offer much more manageable.

Here are our top 4 organization tips to get organized:

Tip #1 - Export your equity from Shareworks

Stripe manages its equity plan through Shareworks. Shareworks isn’t perfect, and we know that some of you really dislike it. But in spite of its flaws, it can do what you need it to do.

The first thing you’ll want to do is export a full record of your equity. The PDF “Shareworks Account Summary” is usually a good place to start. There should be a CSV export option as well.

This data export should provide you with a detailed view of your equity that includes each grant, the type of equity owned, the grant date, the number of shares/units, your cost basis, and all your previous transactions by equity type. (Borderline too much information.)

Tip #2 - Organize first by equity type

The export from Shareworks should do most of this for you, but you’ll want to make sure you structure your data by equity type first.

At this point, most people at Stripe have RSUs and RSUs only, but if somehow you still have ISOs, NSOs, or shares that are QSBS-eligible, you’ll want to make sure you’re separating them out by each type since there are different tax consequences for each.

Tip #3 - Organize by cost basis and vest date

Again, the Shareworks export should do most of the heavy lifting here, but you’ll want to consolidate the information in a way that makes it easily accessible and understandable to you.

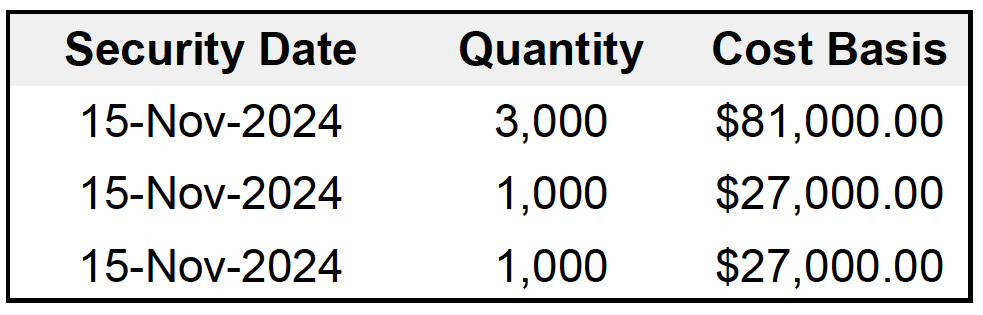

When you export a detailed report from Shareworks, it will likely break out each grant separately and will show multiple lines for the same vest date. It can look like this:

You can choose to leave the extra detail, or you can collapse the information into one line. You’ll just want to make sure you’re not combining mismatched vest dates and/or cost basis information. Here’s how you can combined the information:

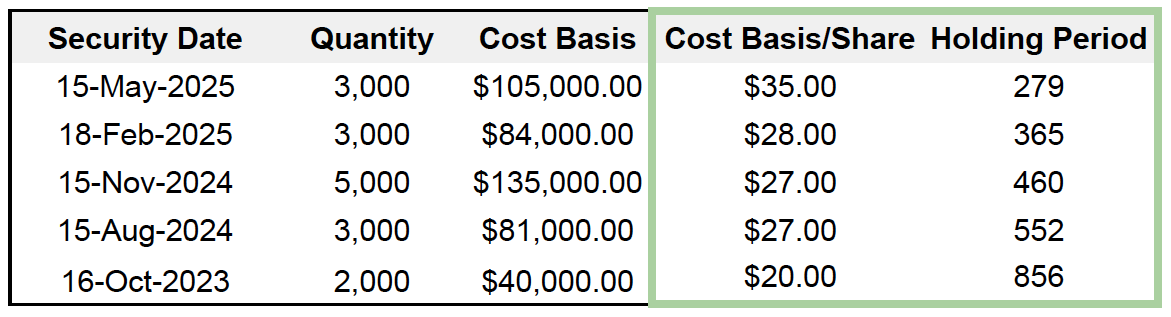

Tip #4 - Track holding period and cost basis per share

The Shareworks export (at least as of the writing of this article) doesn’t provide you with the cost basis per share or the exact holding period from the time the report was generated. It does provide you with the data to do it yourself, but it doesn’t provide you with that number as a separate column.

You will need to know both of these figures if you want to optimize your Stripe tender offer. Here’s how it would look if you were to add those two columns to the data set.

You’ll need both of these pieces of information because they allow you to (1) figure out which Stripe shares to sell and (2) determine what the tax consequences of selling will be.

Proper Tax Assumptions for Stripe Tender Offer

Now that you’re organized, you’re ready to start thinking about how taxes are going to impact you when you go to sell your Stripe equity.

It never feels good to look at the taxes you’ll have to pay, but it’s a necessary part of the math equation to figure out your strategy for the tender.

Tax Assumptions for RSUs

Since Stripe no longer has double-trigger RSUs, your RSUs are taxed at vest, and will be taxed again at sale (assuming you sell at a gain). This “taxed at sale” part is the part that is most applicable at Stripe’s tender offers.

Depending on how long you’ve held your shares following the vest date, selling at a gain will result in either a long-term or short-term gain.

If you’ve held your shares for longer than 365 days, you have a long-term capital gain.

If you’ve held for 365 days or less, then you have a short-term capital gain.

Long-term capital gains are taxed at long-term capital gains rates, state income tax rates (if applicable), and potentially NIIT (Net Investment Income Tax) as well.

Short-term capital gains are taxed at ordinary income tax rates, state income tax rates (if applicable), and potentially net investment income tax (NIIT).

Below are the tax tables for ordinary income tax rates and long-term capital gains. If you live in California and are in the highest tax brackets, you’ll likely be paying the following:

Short-term Capital Gains

37% Federal tax

3.8% Net Investment Income Tax (NIIT)

13.3% California tax

Long-term Capital Gains

20% Federal tax

3.8% NIIT

13.3% California tax

Tax Assumptions for NSOs and ISOs

Our assumption is that you’ve probably already exercised any options that were previously granted. Assuming that’s the case, they’re basically just shares at this point. (There are some differences with ISOs, which we’ll discuss briefly.)

That said, it’s worth mentioning that in the case of NSOs, if you haven't yet exercised, exercising is what creates the first taxable event (just as it does when RSUs vest), and selling creates the second.

If you wait until a tender to exercise and sell, you’ll simply be paying ordinary income taxes on the difference between your exercise price and the tender offer price.

In the case of ISOs there are very few folks at Stripe with ISOs left to exercise, and realistically, probably none. At this point, exercised ISOs should meet the requirements for a qualifying disposition. If you happen to be one of the few who do have ISOs, please read our When to Exercise ISOs article for more education.

Estimate Tax Cost per Stripe RSU

Once you’ve established some tax assumptions for your RSUs based on the unrealized gain and holding period, it’s often worthwhile to determine the tax cost per RSU/share sold.

This is particularly helpful to review if you had Stripe RSUs vest close to the date of a Stripe tender offer.

Since long-term capital gains rates are lower, people assume they’ll result in the least amount of tax paid, but that’s not always the case. RSUs that recently vested could have a short-term capital gain, but the tax may be less than if a share were sold from an earlier vest.

For example, if you have 1 RSU at a $30 long-term capital gain and 1 RSU with a 1 dollar short-term capital gain, selling the RSU with a short-term gain results in more cash to you vs taxes paid. (Not saying this is what you should do, but it’s something to review.)

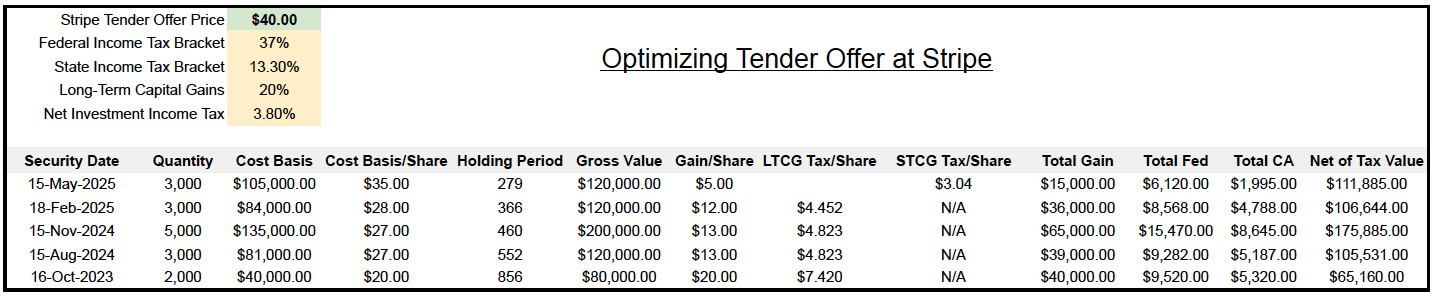

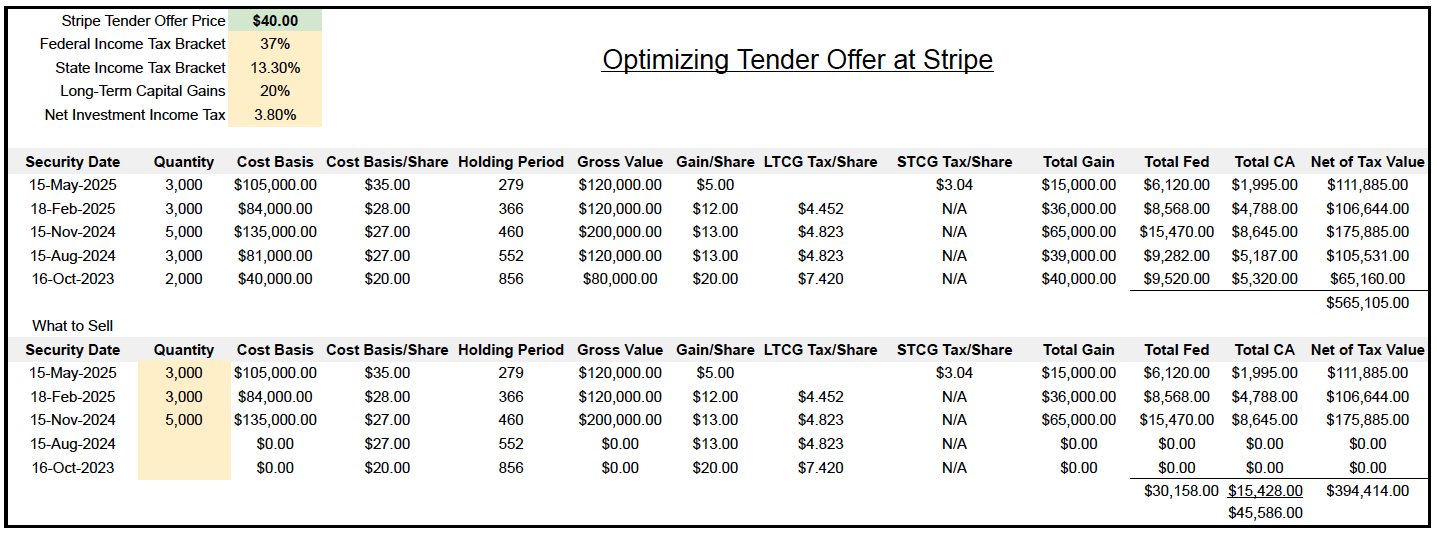

Example Spreadsheet Ahead of Stripe Tender

To help you envision what it looks like to compile the information in one place, we’ve included a screenshot of how we like to organize everything for our clients. (We’ve obviously changed the values of share prices and tender values.)

While the spreadsheet itself isn’t much to look at, it does create a clear picture of (1) how much Stripe you own after-tax, (2) how much Stripe would need to be sold to end up with a certain amount, and (3) helps you determine which Stripe shares to actually sell.

To take it one step further, we often copy-paste all the organized information so we have a place to easily look at what happens if we choose to sell differing amounts from each vest date.

Putting everything into a place that allows you to easily manipulate the information is helpful for more than just tax planning reasons. It’s also helpful because you can start to visualize what you can do with your Stripe dollars.

Determine How Much Stripe Needs to be Sold

One of the funnest parts of guiding people through tender offers is helping them figure out how much Stripe they need to sell to accomplish their current and future financial goals.

The amount that someone decides to sell in a given tender is completely personal to the individual and requires some thought on things other than taxes and investments.

Regardless of the size your Stripe position has grown to, it’s helpful to think about what’s actually important to you about the wealth you're building.

This is a non-exhaustive list, but some things we’ve helped clients think through are:

How much needs to be sold for me to retire?

How much needs to be sold for me to be able to CoastFIRE?

Should we buy a house with what we sell? What kind of house purchase can we afford?

Should we diversify investments outside of Stripe since Stripe has grown so much?

If we sell X amount, how do we account for taxes? When do taxes need to be paid?

If I’m projected to owe estate taxes someday, what things should I be doing now to avoid estate taxes?

Would moving out of California help with any of this?

The list can go on and on. Ultimately, you want to build some sort of decision-making framework that helps inform your decision whether to sell or not. You shouldn’t be selling just to sell; you should have some rationale behind the sale.

Example Output of Financial Planning

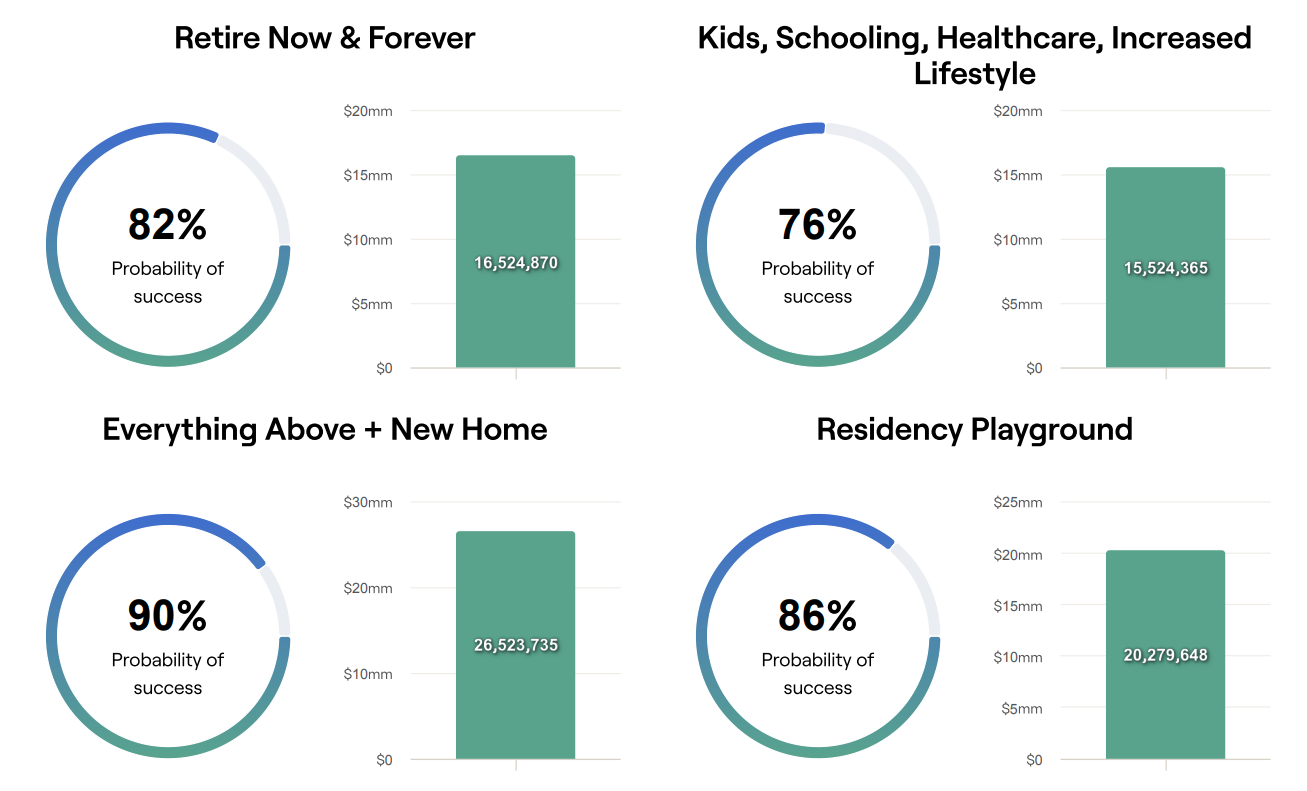

We use RightCapital to help us build out financial planning models for clients. The output of the tool isn’t the end all be all, but it does help build a framework for making decisions.

In this example, we have a client who wanted to see how much stock needed to be sold at a tender in four different scenarios.

Retire now and forever

Retire now and forever, but add more expenses plus kids

Everything above, but add a new home

Evaluate how moving to a new state could impact things

Within each scenario, we are able to evaluate just how much equity needs to be sold to put us on the right path based on a given set of assumptions.

Even if you don’t use this tool, there are plenty of other awesome free ones online. We highly recommend that you build your own financial plan for yourself. Even if it’s super rough, it helps put your tender offer decision in the context of your bigger picture.

Making Equity Selections for Stripe Tender Offer

Once you’ve done everything above, you’re ready to make selections for how much and what Stripe shares to sell.

It’s important to note that while you may be ready, you will have to accept the fact that you will never be able to perfectly optimize what ultimately happens with your Stripe equity, and that’s okay.

If you’ve created a good game plan, you’ll be able to live your life without regret.

As far as the actual selections go, this is where you’ll go back to your neatly organized spreadsheet of Stripe equity and make the final call on what to sell.

For the rough ordering, you’ll typically want to sell the batches of shares that result in the least tax cost until you arrive at the number that you’d like to sell.

That said, if you’re planning on holding shares, there’s an argument that it’s okay to just hold your shares that are at a short-term capital gain until they’ve reached long-term capital gain status. (It’s kind of a preference thing.)

Tax Plan Following Stripe Tender Offer

What you decide to do with Stripe tender proceeds needs to include a plan to eventually pay taxes. Here are some quick guidelines for making a good tax plan with the proceeds:

#1 - There is no withholding when selling Stripe shares

When you sell your Stripe shares, there’s not an automatic withholding that happens like when your RSUs vest. You are required to hold the cash needed to pay the taxes generated from long-term and/or short-term capital gains.

#2 - You should know estimated tax payment rules (at least roughly)

The IRS has rules for how much tax needs to be paid throughout the year. If you don’t pay in at least the expected amount, you’ll be assessed penalties when you file your taxes.

If you’re a high earner, the IRS wants you to pay in at least the lesser of either:

110% of your prior year’s total tax

Or, 90% of your current year’s total tax

If this is your first tender offer, it’s likely that paying in 110% of your prior year’s total tax is the method you’re going to use.

If you paid $200k in Federal taxes in 2025, then in 2026, the IRS expects you to pay in $220k throughout the year or $55k per quarter. If you pay this correctly, then no matter how much you owe on April 15th, you won’t be assessed tax penalties. (Which is important for the next bullet.)

California has similar rules to Federal, but also some material differences for people with income and gains of over $1M. California typically requires you to pay in 90% of your current year’s estimated taxes throughout the year, though there are some exceptions to penalties.

We’ve written about how to avoid underpayment penalties in California before. More information can be found there.

#3 - Pay in what’s required and earn interest on the rest

If your tax bill gets big enough, properly hanging onto your cash can earn you tens of thousands of dollars. You don’t get any sort of thank you from the IRS for paying all of your taxes early.

The biggest strategy for Federal taxes is to meet the safe harbor requirements and set aside the remaining taxes owed in some sort of high-yielding cash fund. This could be a high-yield savings account, money market funds, or treasuries.

We oftentimes will use Treasuries because they avoid state income taxes, which results in a better after-tax yield on the cash.

#4 - Save taxes where you can

Tax avoidance is legal, tax evasion is not. If you sell millions worth of Stripe during a tender, it will be very tempting to do all you can to avoid taxes. We’ve seen some really interesting ideas come through the door over the years.

As a W-2 employee, the reality is that you’re limited, but hitting all the basic things can add up pretty significantly.

Maxing your 401k, doing an HSA, doing a dependent care FSA, harvesting losses, bunching charitable contributions, and donating stock to a DAF are the big ones you can look out for. We’ve written an article about how to avoid taxes on RSUs, and it covers most of the strategies that would be available to you at a Stripe tender offer.

The tax saving ideas that float around on social media that seem too good to be true, we highly recommend chatting with a tax professional before you YOLO your way into an audit.

Final Thoughts on Optimizing Stripe Tenders

People may not realize this, but Stripe's offering of tender offers on a regular basis has set the example that many other private companies now follow with their tender offers.

Even though there have been a handful of Stripe tender offers, each one creates a unique opportunity for you to improve your financial position and turn Stripe equity into something meaningful to you. It helps that the stock price keeps going up like crazy of course!

If you want help thinking through how to make the most of a tender offer at Stripe (or any company), we’re happy to chat with you. We’re unique in the sense that we are advice-only, which may be a better fit for clients making decisions around how much company stock to sell or not sell.

Thanks as always for reading!