What to Do With RSUs at IPO

IPOs are cause for a lot of excitement. Outside investors who’ve been wanting to purchase company equity can finally get a piece of the pie and company insiders who own a lot of company stock finally have an opportunity to sell shares. Employees holding RSUs have a long list of things to consider once their company IPOs.

There weren’t many IPOs in 2022, 2023, or 2024. But this means that there’s pent-up demand and lots of people wondering what to do with RSUs once their company eventually IPOs.

Whether your company is planning to IPO in 2025 or 2026, what to do with your company’s RSUs at said IPO is a topic worthy of consideration.

This article will provide you with 10 things to keep in mind when managing RSUs at IPO. We’ll provide 4 risks to look out for and 6 other thoughts/recommendations we feel will help you be successful in managing your RSUs through an IPO.

RSUs at IPO Risk #1 - Tax Withholding Preferences

If a company is already public, RSUs are usually taxable when they vest. If RSUs vest while you’re at a private company, they usually won’t be taxed until your company goes public or is acquired (this is called a double-trigger RSU).

If you’ve been at your company for awhile and have received RSUs, you could find yourself with a substantial amount of money that will become taxable at IPO - meaning you’ll owe substantial taxes.

To help you figure out this RSU tax issue, companies sometimes offer employees one or more of the following options:

The company could pay your tax withholdings for you - Your company might be willing to cover taxes until the lock-up period following an IPO has passed (normally 90-180 days). They’ll charge you a little bit of interest, but it allows you to continue holding company shares rather than letting some go to pay taxes immediately.

The company sells shares/RSUs to cover taxes for you at IPO - (This is our preferred option.) Your company will sell shares to cover tax withholdings at the initial IPO price. The pros are that shares are being sold before the lock-up period ends, you’ll know what price you’re going to get, and it protects you if the value of the company drops immediately after the IPO. The con is that if the stock goes up immediately after the IPO, you’ve sold shares and missed out on gains.

You can wire the company the tax withholding money - This one requires quick action around the time of the IPO. Once the IPO price has been finalized and your taxes have been calculated, your company will give you wire instructions to send them money so you have proper withholdings.

No matter how many RSUs you’ve been granted, you’ll want to understand (1) the general taxability of your vested RSUs at IPO and (2) you’ll want to make a plan to ensure you’re setting aside cash for taxes.

Note: If you don’t know much about the RSUs you’ve been granted, we recommend reading our RSU Basics article. After that, it may be a good idea to brush up on when do you owe taxes on RSUs. We’ve also built an RSU Tax Calculator that is free to use and can help you get a better guess at how much you’ll owe in taxes.

RSUs at IPO Risk #2 - Lack of Tax Withholdings

If you’re a high earner, there’s a very good chance that your company will not withhold enough taxes for you. This is a big potential pitfall!

Unless you’re earning over $1 million at your company, they’ll likely withhold at the following rates:

Federal - 22%

California - 10.23%

Oregon - 9%

Utah - 4.95%

Other States - We don’t know off the top of our heads :)

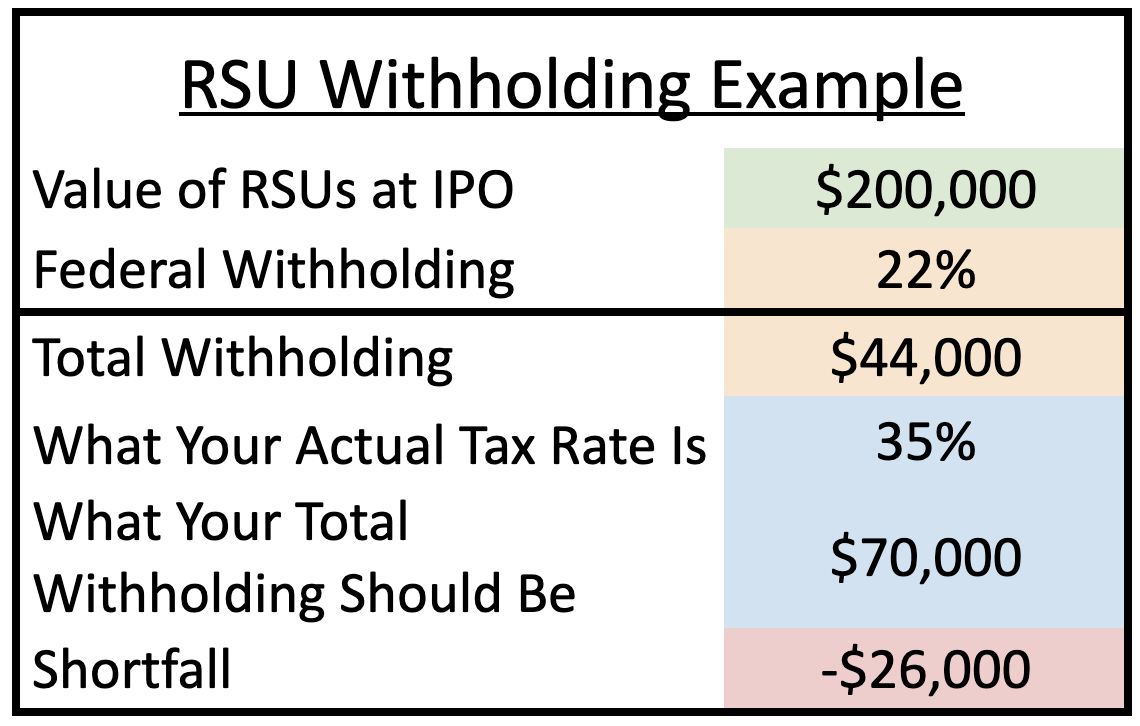

Let’s say you’re single and make $180k. You also have $200k of vested RSUs that are going to become taxable at your company’s IPO. Here’s what that looks like for Federal taxes:

In this example, if you had $200k in RSUs become taxable at IPO, you would have been underwithheld by $26k.

This is important because (1) it’s $26k you may not be aware of and that you’ll now have to pay the IRS, (2) you could be incurring penalties for not withholding enough tax throughout the year, and (3) this same issue could be happening with state income taxes.

RSUs at IPO Risk #3 - Where the Stock Will Go After IPO is a Mystery

Plenty of well-known companies have sputtered immediately after IPO. Companies like Eventbrite, Survey Monkey, Lemonade, Slack, Lyft, and Dropbox all underperformed following their IPO. Most have not rebounded and it’s been a couple of years.

You can gamble as much as you’d like, but it’d be wise to ensure that, at the very least, you have your taxes covered before you bet everything on red or black.

Rivian exploded after the IPO, but has since pulled back considerably. It’s very likely that employees at Rivian locked in a tax liability at high prices, but never sold enough shares to cover their tax bill. Now people in this situation might need to sell shares at depressed pricing to cover what they owe.

What you want to avoid is owing taxes and not having the means to sell and raise enough cash to cover taxes.

RSUs at IPO Risk #4 - Your Net Worth = Your Company RSUs

The greater percentage of your net worth your RSUs make up, the greater swings you'll see in your net worth. After an IPO, company stock can move quickly in either direction. Many people will only experience one liquidity event (IPO) and if you don’t move a portion of money away from your company, you may miss taking full advantage of the opportunity.

We’ve written an article discussing how much company stock is too much and people have found it helpful when determining how many RSUs to sell at IPO.

6 Recommendations to Manage Your RSUs at IPO

As with all things, DIY is great until things get too complex. This is especially true with tax and investments. A company going public is certainly a time when you may want to consult with experts to discuss your specific scenario.

We’re happy to lend a helping hand and are happy refer you out to people that will have your best interest at heart. Most places we refer our readers to are happy to do one-time engagements, but if you’re looking for a long-term advisor, we can provide that as well.

All that said, we’ve helped a lot of people go through liquidity events and have some good insights to ensure you’re thinking about the right things when a company is about to go public.

#1 - Determine Your Current Financial State

In order to make the most of your RSUs, you’ll need to get a solid understanding of your current financial state. You’ll want to think about all of your assets, all of your debts, and upcoming future expenses. After you’ve evaluated those things, you’ll want to think about how you can best use the RSUs.

Here’s a list of things you may want to consider:

Do you have any car loans?

Do you have any student loans?

Do you have any credit card debt?

How much of an emergency fund do you have?

Do you have any investments besides your 401(k)?

Do you want to save for a house?

Do you have upcoming medical expenses?

Do you want to save for a child?

What percent of your assets do your RSUs make up?

This list could be endless, but the point is that your evaluation should be thorough.

Regardless of how you answered the questions above, the RSUs you have will make some kind of difference in your current financial state. In this linked article, we discuss the best uses of RSUs proceeds. As long as you’re being intentional and not taking excessive risks, you’ll likely be in a good spot.

#2 - What Are You Okay Losing or Giving Up?

Ask yourself this question, because if you don’t figure out the answer, you could end up losing a lot of sleep over your decision to sell some RSUs at IPO or not.

How much will you hate yourself if you sell everything and your company skyrockets? What are you risking if that happens?

How sad will you be if you don’t sell any and the company drops 50% after IPO? What are you risking if that happens?

Is there an amount you can sell that will enable you to stomach whatever happens in the future?

There are times you can have an extremely positive outlook, extremely negative outlook, or even a completely neutral outlook. No company is the same and no individual is the same (every employee is different). Whatever you decide to do with your RSUs, it should align with your financial goals.

#3 - If RSUs = Your Net Worth, Consider Diversifying

There’s a saying, “Concentration builds wealth, diversification preserves it.” If this is your first liquidity event, your material net worth is probably made up mostly of your employer stock. That’s fine for a time, but leaving your material net worth tied up in one single stock is a recipe for massive swings, up and down.

We don’t love blindly following rules of thumb, particularly since everyone has different circumstances. Many ,“Don’t hold more than 10% of your net worth in a single holding.” This is good advice generally, but if you want to hold 15-20% of your net worth in your company stock, you probably can get away with it if you have a good rationale.

#4 - RSU Tax Withholding Preferences

IPOs from 2020 and 2021 brought even more tax withholding scenarios than those previously mentioned above. Some companies have tried at some new ways to cover the tax withholdings.

Ideally you want to complete all of your withholdings at the same time your RSUs become taxable to you (which is usually the IPO date). This takes a lot of risk off the table immediately and will give you a benefit before your lock-up has expired.

#5 - Determine Potential Tax Underwithholding

If you're already at a pretty high salary and your company is going public, be sure to chat with your CPA and communicate that you might be underwithheld. If your company gives you an option to withhold at a higher rate, it should be a strong consideration to do so. By withholding at a higher rate you’ll get an immediate benefit of using vested RSUs to cover that withholding.

If you don’t want to talk to a CPA, you can do some back-of-the-napkin math by taking your salary and then adding in your RSUs that will be vesting. You’ll want to see what tax rate is being applied to each RSU that vests. If you’re above the 22% tax bracket, you’ll want to prepare to pay additional taxes in April.

#6 - Glance Back, Don’t Keep Looking Back

Once you’ve executed on a decision, own it. There are so many variables once a company goes public that there will always be something you could have executed better and/or more money you could have made. Glancing back into the past is fine to ensure you learn a lesson, but don’t keep looking back and dwelling on missed opportunities.

If you’ve read to this point, it’s likely that you may have some questions or past experiences you’d like to share. Please leave your comments below and we’ll be sure to comment/include your thoughts.