Correct Math on ESPP Qualifying & Disqualifying Dispositions

Employee Stock Purchase Plans (ESPPs) are one of our favorite topics to write about. They can provide a tremendous boost on your path toward financial independence when you use them correctly. Unfortunately, problems can arise when people don’t understand the differences between an ESPP qualifying disposition and an ESPP disqualifying disposition.

Nothing pains us more than seeing tax math errors made on both of these disposition types. ESPP mistakes happen all too frequently, even on really great sites, and with really great advisors.

We’ve written about both subjects separately before, but figured it’d be helpful to write a longer, more detailed article discussing the calculation differences between the ESPP Qualifying Disposition and the ESPP Disqualifying Disposition.

What is an ESPP Qualifying Disposition?

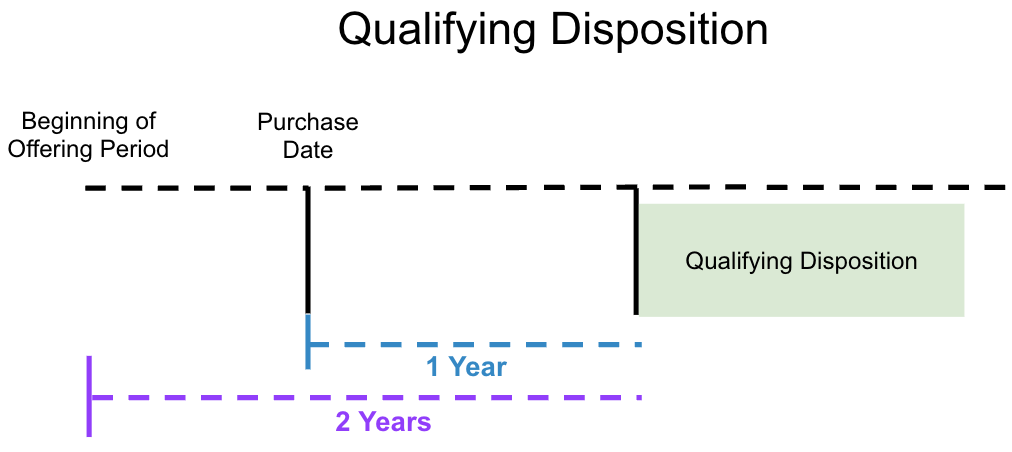

A Qualifying Disposition on an ESPP requires that you hold the stock you purchase through an ESPP for two different periods of time:

Hold for one year after purchasing your stock.

Hold for two years since the start of your ESPP’s Offering Period (assuming there’s a lookback).

The first requirement is really straightforward. After purchasing your stock through an ESPP, you need to hold that stock for a full year.

The second requirement is a little more complicated and can vary based on the company you work for.

The offering period is the length of time the ESPP will run for. The offering period will be followed by another, then another, then another… and these offering periods can vary in length.

The most common length for an offering period is 6 months, but it can be up to 24 months.

Examples of ESPP Qualifying Dispositions

Here’s a simple illustration of what an ESPP Qualifying Disposition can look like. (There will be plenty more illustrations later, so please stay with us as we explain.)

As you can see in the illustration, two things need to happen if you’re shooting for a qualifying disposition: (1) you need to hold for at least two years since the beginning of the offering period, and (2) you need to hold for one year since the purchase date.

It may seem like a small thing to track, but knowing whether you’re going to have a Qualifying or a Disqualifying Disposition can mean the difference of several thousand dollars in taxes.

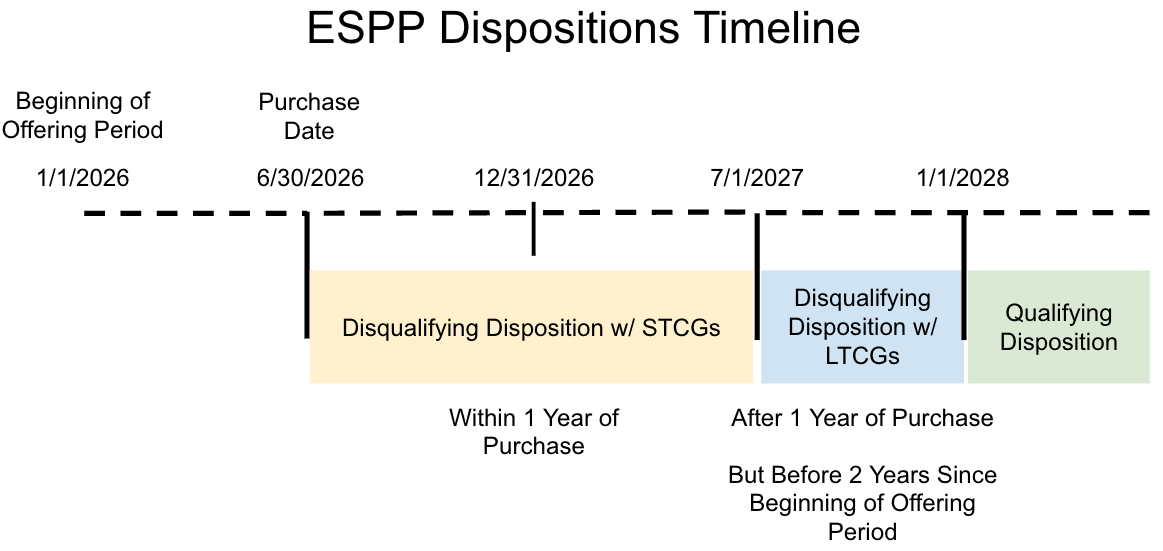

What is an ESPP Disqualifying Disposition?

A Disqualifying Disposition of your ESPP shares is any disposition that doesn’t meet the requirements of a Qualifying Disposition.

So either:

You sold sooner than one year after purchasing ESPP shares.

You sold sooner than two years since the start of your ESPP’s Offering Period.

This is where ESPPs can start to get a little weird. If you re-read the disqualifying disposition triggers, you can see that it’s possible to accomplish #1 while failing to achieve #2.

This possibility creates two potential disqualifying disposition types.

Stock held for more than a year is considered a Long-Term Capital Gain (LTCG), and anything held for less is considered a Short-Term Capital Gain (STCG).

Depending on when you sell and create a disqualifying disposition, you can end up with either a (1) Disqualifying Disposition with Short-Term Capital Gains (STCGs) or (2) a Disqualifying Disposition with Long-Term Capital Gains (LTCGs).

Here’s a graphic to help illustrate:

We’ll get into the specifics of taxes soon, but this creation of a Disqualifying Disposition with Long-term Capital Gains is one of the reasons why it’s not always best to have a pure Qualifying Disposition.

Types of Income, Gains, and Tax Rates

There are other classifications of income than just this, but the types of income and gains as it relates to your ESPP are:

Ordinary Income

Short-Term Capital Gains

Long-Term Capital Gains

Ordinary Income is taxed at ordinary income rates. Here’s a link to a table of the tax rates.

Short-Term Capital Gains (STCGs) are taxed at ordinary income rates as well. In addition to ordinary income, you may also owe Net Investment Income Tax (NIIT) as well.

Long-Term Capital Gains (LTCGs) are taxed at long-term capital gain rates. Here’s a table of LTCG tax rates. LTCGs are potentially subject to NIIT.

If you’ve read our other articles, all of this is probably a refresher for you. But it bears repeating, so we establish a baseline before getting into the weeds of ESPP Qualifying and Disqualifying Dispositions.

Calculating Income and Gains of Each Disposition Type

No taxes are owed on a qualified ESPP at purchase. You only create taxes at the sale.

Calculating the income from ESPP Disqualifying Dispositions is a little easier to understand, so we’ll start there.

Calculating Ordinary Income and Gains From a Disqualifying Disposition

There is always going to be an ordinary income element if you sell your ESPP shares in a disqualifying disposition. This is true, even if you sell at a loss.

The ordinary income portion of an ESPP is determined by taking the Fair Market Value (FMV) at the time of purchase and subtracting it from the discounted price you actually paid for your shares.

Anything above the FMV at purchase will either be a short-term gain or a long-term capital gain. And anything below will be a capital loss.

The next several sections provide examples/ illustrations with various disqualifying disposition types based on what happens with the stock price.

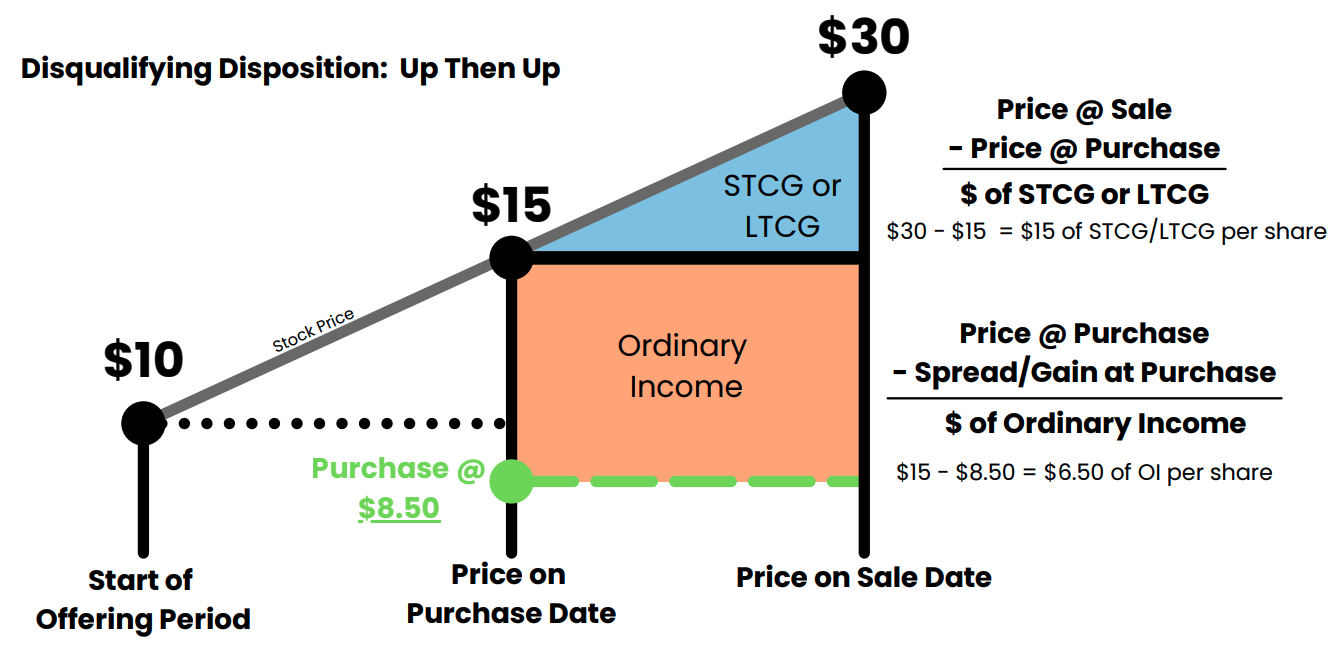

ESPP Disqualifying Disposition Example #1 - Up Then Up

In this disqualifying disposition example, the stock price only goes up from the beginning of the offering period to the purchase date, until the eventual sale date.

To determine the amount of ordinary income in a disqualifying disposition, you don’t look at what the price is at the time of sale at all. You look back at what your gain was at the time of purchase.

In this example, the stock price at purchase was $15, and because you paid $8.50 for the stock, you locked in $6.50 per share of ordinary income.

This $6.50 of ordinary income will remain no matter what the ultimate sale price is, so long as it’s a disqualifying disposition.

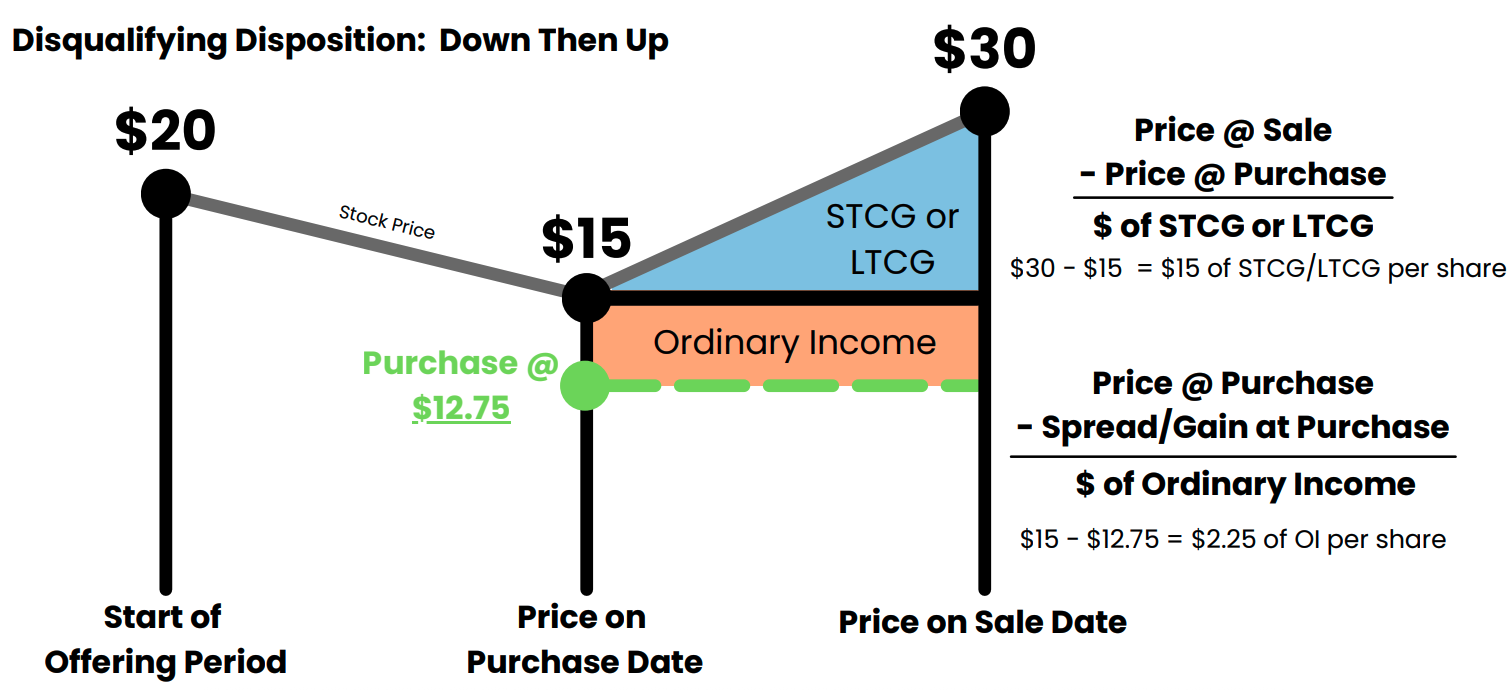

ESPP Disqualifying Disposition Example #2 - Down Then Up

In this disqualifying disposition example, the stock price starts high, then drops, then goes up above the price at the beginning.

The price in this example goes from $20 to $15, and shares are purchased at $12.75 per share.

Regardless of what the sale price ends up being, on a disqualifying disposition, the ordinary income per share in this example will be $2.25 per share.

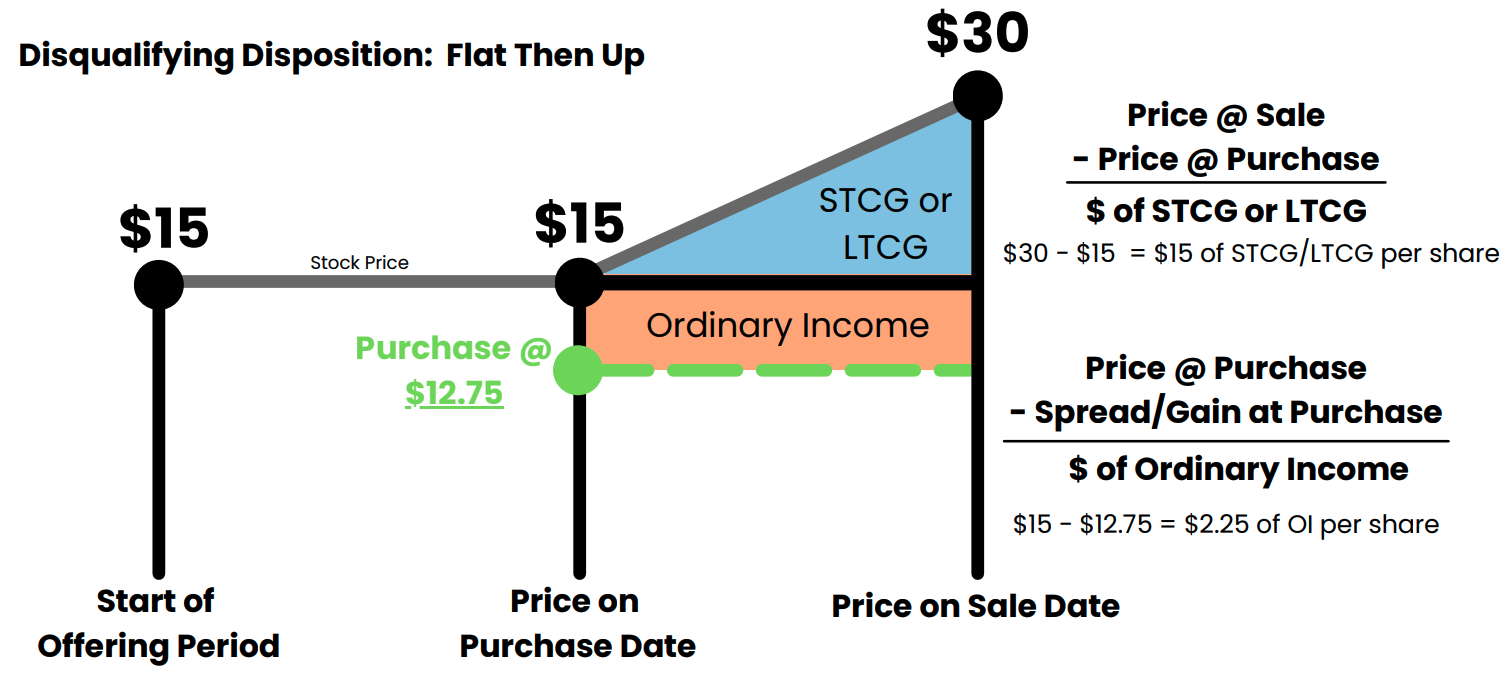

ESPP Disqualifying Disposition Example #3 - Flat Then up

This example is pretty similar to the previous one, but we’re including it just so you can see another combination that might help the math “click” for you.

In this example, the price stayed the same from the beginning of the offering period to the time of purchase.

Shares are purchased for $12.75 when the shares were actually worth $15 per share at purchase.

This means the same thing as it did in the previous examples. So long as this is a disqualifying disposition, the ordinary income portion will be $2.25 per share, no matter what the sale price is.

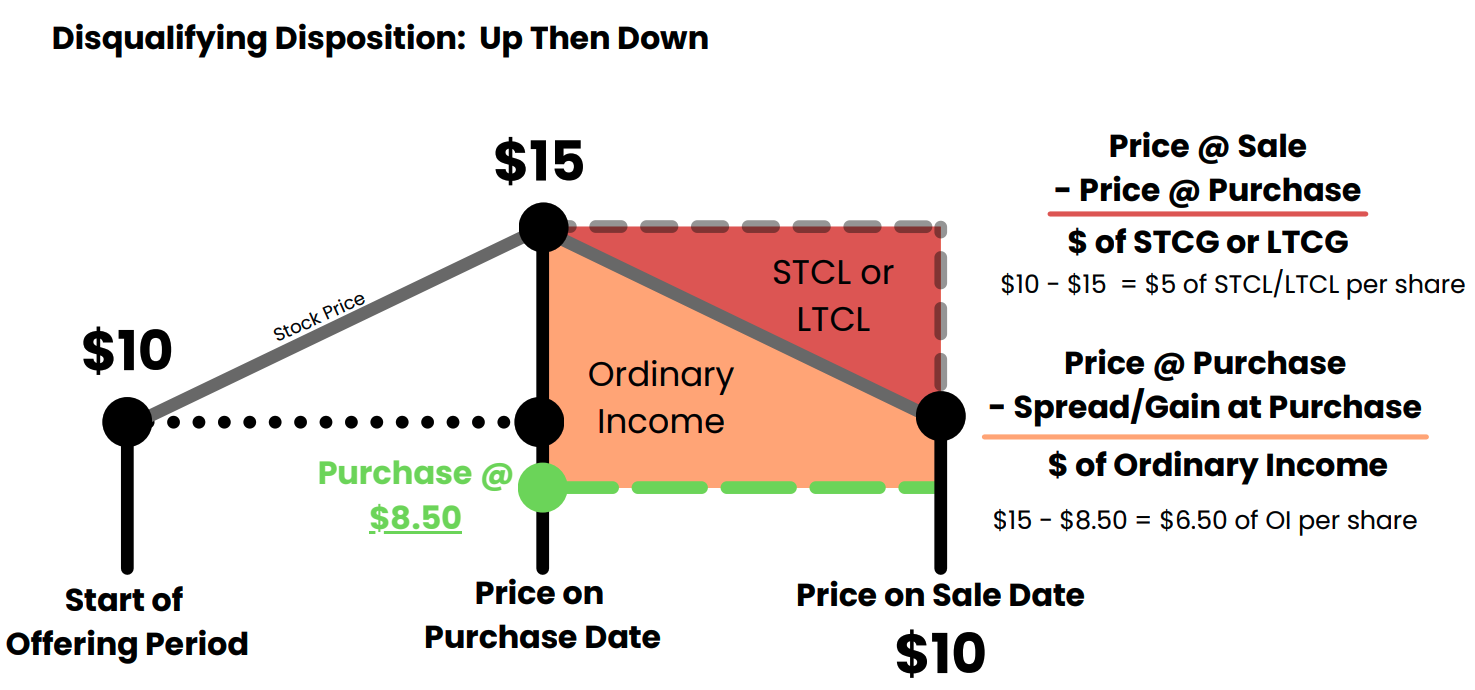

ESPP Disqualifying Disposition Example #4 - Up Then Down

This next scenario is less fun than the other scenarios. In this scenario, we’ll look at what happens if you have a disqualifying disposition and the stock price goes up, then comes back down after you make a purchase.

The stock price started at $10, at purchase the stock was worth $15. This means you purchase shares at $8.50.

Just like in the other examples, so long as you have a disqualifying disposition, your ordinary income portion will be set at the purchase date.

In this example, the stock price drops after purchase. You might think that means you don’t have as much ordinary income, right? No, it means you have both ordinary income AND a capital loss.

In this case, you have ordinary income of $6.50 per share ($15 minus $8.50) regardless of what you sell for, even if it’s at a loss.

You take the stock price you sold for minus the stock price at purchase. And that’s your capital loss.

This is probably the hardest example of the ESPP disqualifying dispositions to wrap your brain around. And it’s another reason why you want to make sure that you’re not paying an ESPP Double Tax by incorrectly entering sale details on your tax return.

Calculating Ordinary Income and Gains on Qualifying Disposition

As if determining what’s ordinary income or gain isn’t difficult enough, qualifying dispositions are actually a little weirder than disqualifying dispositions.

When referring to ESPP Qualifying Dispositions, people often mistakenly say, “You pay ordinary income taxes on your discount.”

That is sometimes true, but it’s not fully accurate. It leaves out important information about what actually happens when you have a qualifying disposition.

The ordinary income element on an ESPP qualifying disposition is the lesser of two things:

The discount from the beginning of the offering period, or

The actual gain realized

The first bullet is what makes qualifying dispositions strange, and is the other factor why sometimes disqualifying dispositions with long-term capital gains are better than qualifying dispositions.

Let’s start with the two easy examples of ESPP Qualifying Dispositions below.

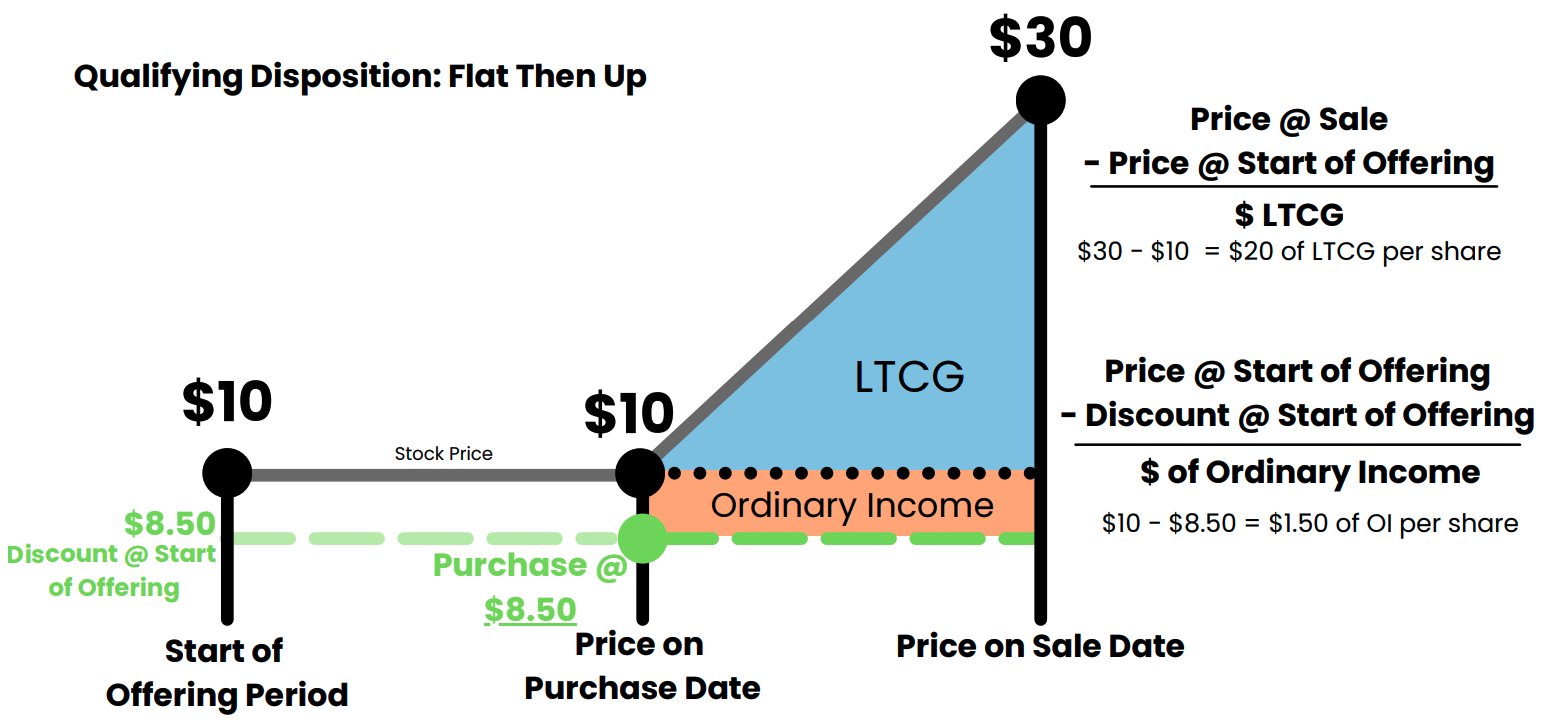

ESPP Qualifying Disposition Example #1 - Flat Then up

This first example assumes the stock price starts at $10, remains at $10 at purchase, then jumps up to $30 at sale.

Assuming all of the above, the ordinary income portion is $1.50, and you’d have a lovely long-term gain of $20 per share.

Unlike disqualifying dispositions, this $1.50 of ordinary income isn’t locked in. It can change based on what the sale price ends up being, which we’ll show in example #3.

First, let’s look at one more simple example:

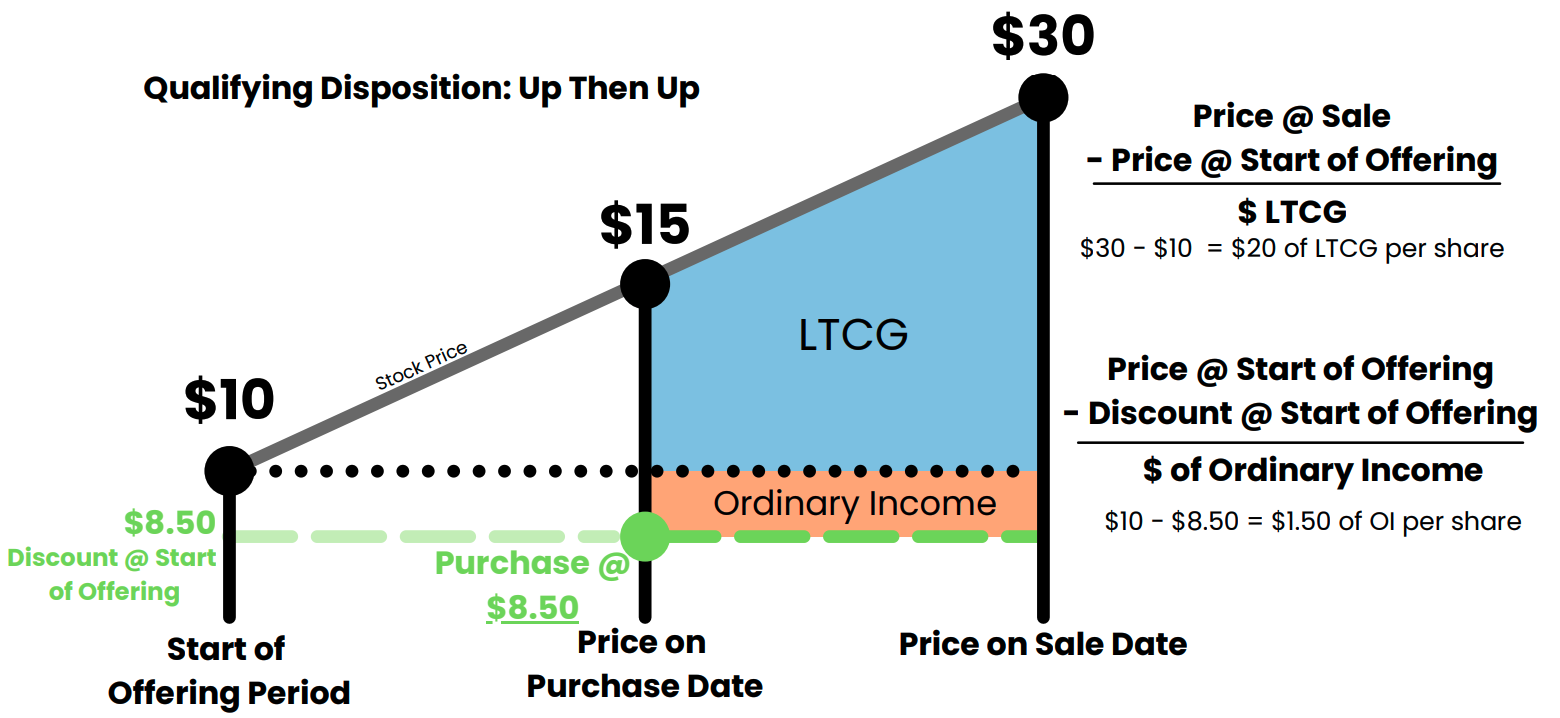

ESPP Qualifying Disposition Example #2 - Up Then Up

This example is what people participating in Apple’s ESPP and Nvidia’s ESPP are used to seeing. Nothing but up and to the right.

Assuming the stock price goes from $10, to $15, to $30, you’d have an ordinary income portion of $1.50 per share and the remaining $20 would all be long-term capital gains.

Again, the ordinary income portion is not locked in. It can change based on what you ultimately sell for.

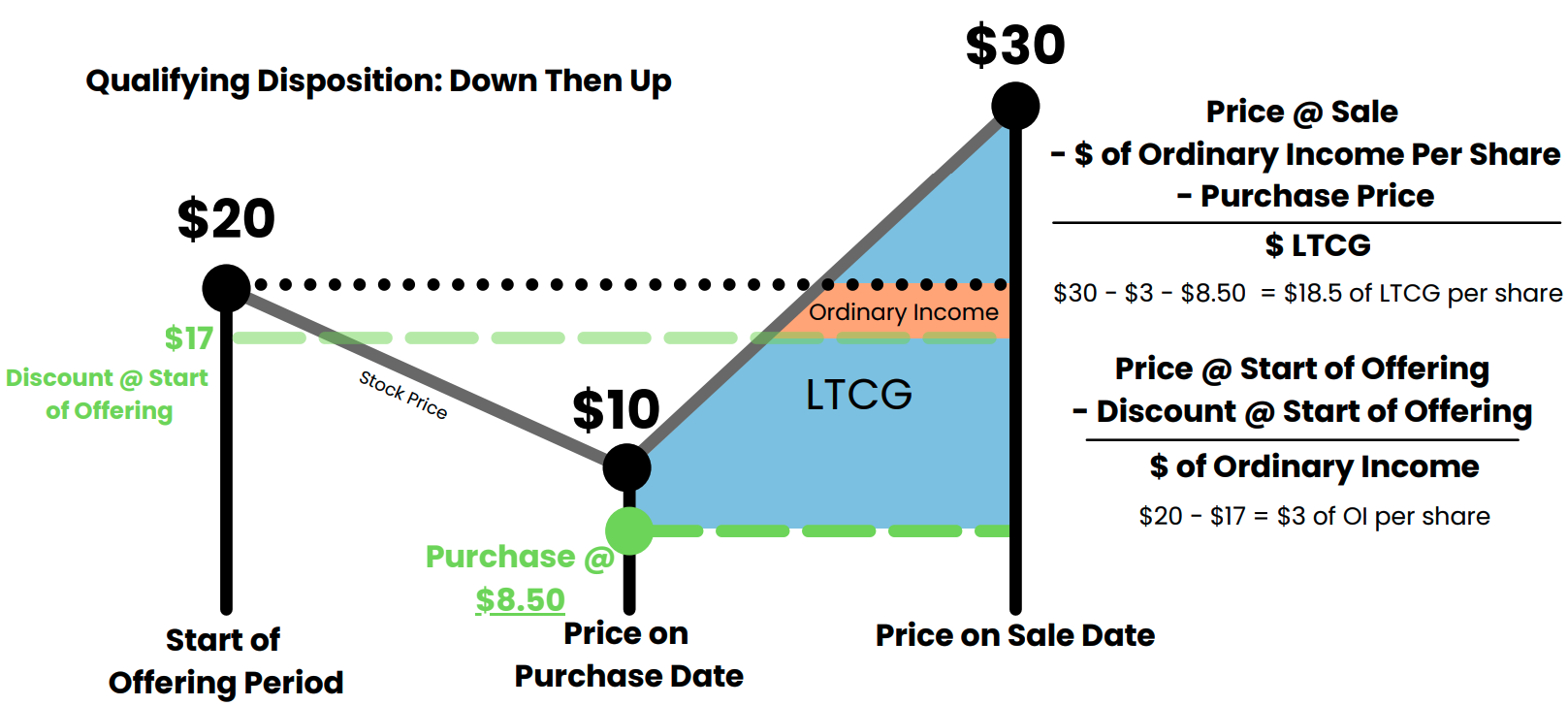

ESPP Qualifying Disposition Example #3 - Down Then Up

The following example illustrates multiple weird things going on:

Assuming the stock price goes from $20 at the beginning of the offering period, to $10 at purchase, then back up to $30, you’d have the following:

Ordinary income of $3 per share

Long-term capital gain of $18.50 per share

The phrase “You pay ordinary income taxes on your discount” is wrong in this scenario.

The ordinary income portion is based on the discount at the beginning of the offering period. This is true regardless of whether or not you ended up using that discount.

This seems like it shouldn’t be true, but this is what so many people get wrong about ESPP qualifying disposition math.

This is also the scenario in which a disqualifying disposition for long-term capital gains will be better than a qualifying disposition. (You’re welcome to play around with our ESPP tax calculator now that you’ve seen some scenarios.)

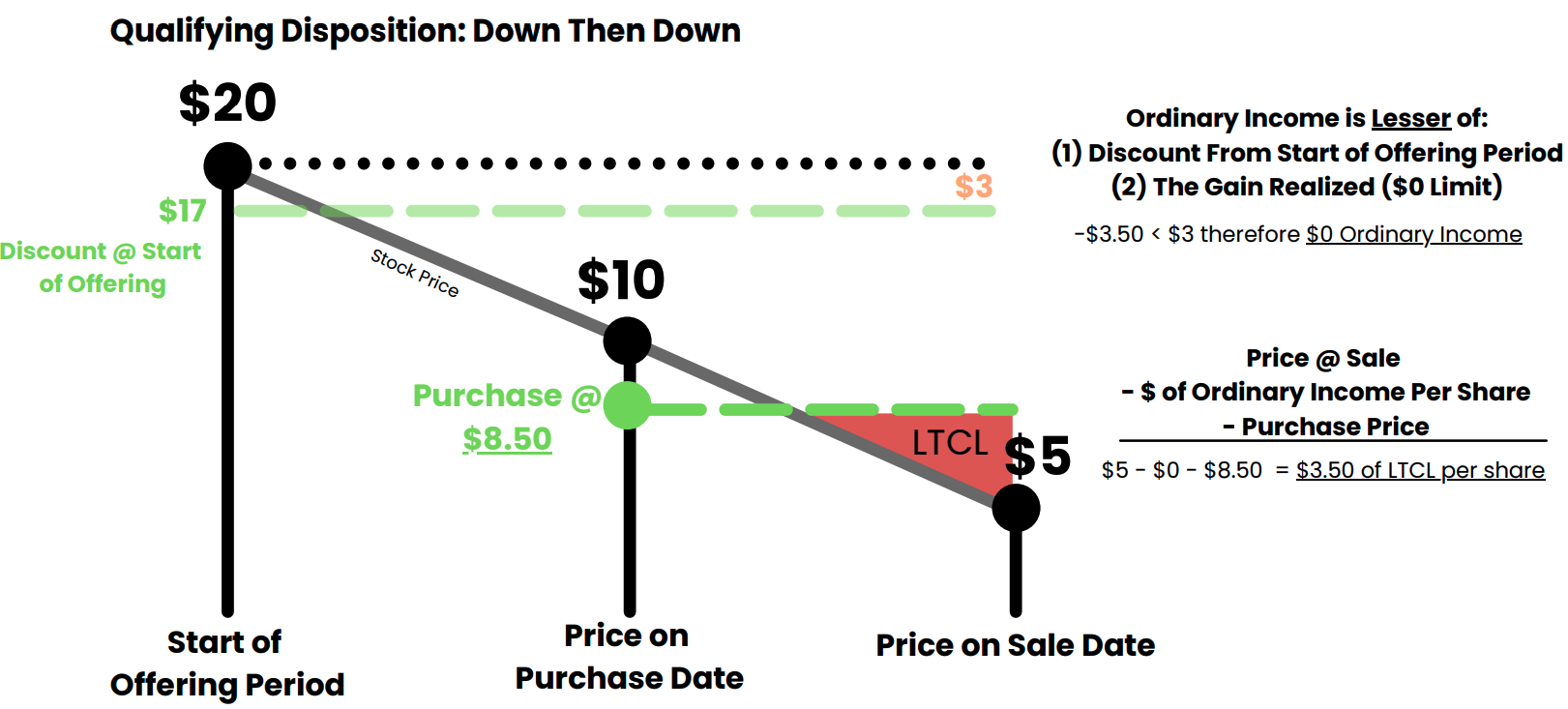

ESPP Qualifying Disposition Example #4 - Down Then Down

This final example is the least fun of the ESPP qualifying disposition examples we’ve shared and is a reason why people often recommend just selling ESPP shares immediately at purchase:

If the stock price goes from $20 to $10 to $5, there are some rules that need to be repeated.

The ordinary income portion is the lesser of (1) the discount as if it were applied at the beginning of the offering period, or (2) the actual gain from the sale.

So in this case, the discount from the beginning of the offering period, even though it wasn’t actually used to purchase the stock, was $3.

The gain from the sale was actually not a gain; it was a loss of $3.50 ($5 minus $8.50).

Negative $3.50 is less than positive $3, therefore, the ordinary income element is $0 (since the ordinary income can’t be negative).

This means that you’d then take the full loss of $3.50 per share and would have $0 of ordinary income.

Concluding Thoughts on ESPP Qualifying Disposition vs Disqualifying Disposition

As strange as it may seem, we really enjoy writing about ESPPs. If structured well, ESPPs are a great way to compensate employees. The downside is that they can be unnecessarily complex, and I would never expect a normal person to want to understand all the ins and outs of an ESPP.

This article wasn’t written to help you decide which disposition to shoot for, or decide if you should max out your ESPP, but rather to make you aware of what can happen when you decide to shoot for either disposition type.

We’ve found that it often makes sense for people to simply lock in their gains and sell their ESPP shares immediately. But if you want to hold onto some company stock, holding ESPP shares can make sense.

Of course, there’s no way to know for sure what will be most beneficial to you because there’s no way to know what your company’s stock price will do in the future. But understanding the factors that influence ESPP dispositions, along with their possible tax implications, can help you make wiser financial decisions and achieve your financial goals.

We hope you’ve enjoyed this ESPP disposition deep dive!